At the end of the day, most of us work for one simple reason: to make a living and build financial stability for ourselves and our families. As someone currently working in international trading while living in Korea under F-4 visa, I usually spend time thinking about contracts, logistics, shipments, compliance, and payment risks. Working hard and building a career are obviously important, but there are also financial matters that foreign workers can easily overlook while focusing on day-to-day business operations. One of those topics is retirement pensions.

So today, I wanted to share what I recently learned about Korea’s retirement pension system from the perspective of a foreign employee.

No matter which industry we work in, salary, insurance coverage, and long-term financial security are all important parts of working life. That is why I recently decided to spend some time understanding Korea’s retirement pension system for employees, especially from the perspective of a foreign worker.

If you are a foreign employee in Korea and work for an employer that properly provides the full package of social insurance schemes — including National Pension, National Health Insurance, Employment Insurance, and Workers’ Compensation Insurance — you are generally covered under the same system as Korean employees, provided that you have the appropriate visa and employment status.

But what about retirement pensions?

Yes, foreign workers can also be entitled to retirement pension benefits under certain conditions.

In general, if you have worked at a company for at least one year and your average working hours exceed 15 hours per week over a four-week period, you may qualify for the retirement pension system.

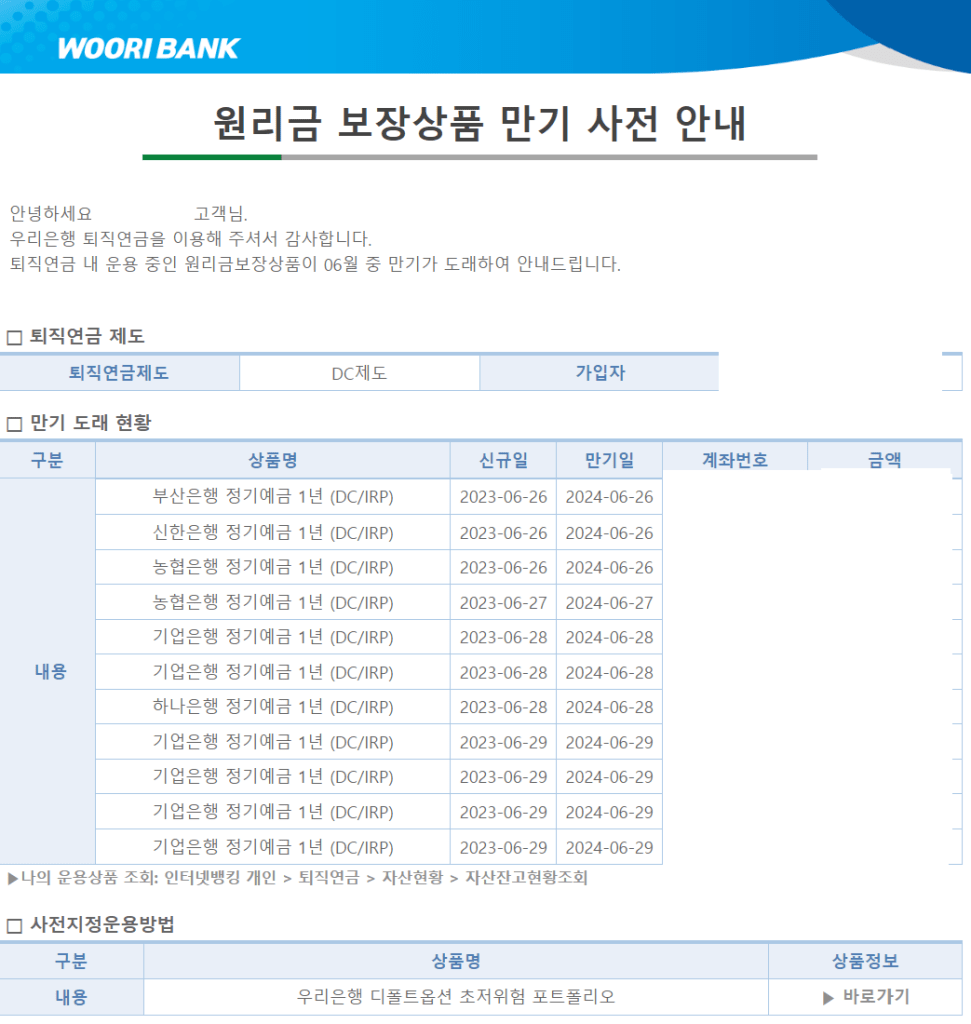

Although finance and accounting topics usually give me a headache, I decided to learn more about the pension plan that my company had originally set up for me. It turned out to be something called a DC Retirement Pension.

What Is a DC Retirement Pension?

DC stands for Defined Contribution.

Under this system, the employer deposits an amount equivalent to 1/12 of the employee’s annual total wage into an individual retirement pension account each year. The employee can then choose how those funds are invested and the accumulated balance will eventually be paid upon retirement or departure from the company.

Can I Withdraw the Pension Before Retirement?

Yes — but only under legally approved circumstances.

Examples include:

- Purchasing your first home

- Long-term medical treatment exceeding six months

- Certain cases involving immediate family members

Can I Contribute Additional Funds?

Yes.

Employees may voluntarily contribute additional funds to the retirement pension account if they wish to increase their retirement savings.

What Are the Pension Payment Conditions?

Generally, pension payments can begin:

- From age 55 or older

- If the contribution period exceeds 10 years

- With pension payments distributed over at least five years

What Are the Advantages of the DC System?

One major advantage is that employees can directly manage their retirement assets.

Because 100% of the retirement reserve is deposited into an external financial institution, employees’ rights to receive their retirement benefits are better protected even if issues arise within the company.

What Happens If You Don’t Manage the Account?

This was actually the part I was most curious about.

For people like me — who are not particularly knowledgeable about finance or investment products — it is possible to leave the system running without actively managing it.

When an investment product reaches maturity, the funds are temporarily operated as a cash-equivalent asset for approximately six weeks. If the employee does not provide new investment instructions during that period, the matured funds are automatically re-invested according to the previously registered default option.

Retirement pensions may not sound as exciting as international trade negotiations or large logistics projects, but they are still an important part of working life — especially for foreign workers trying to build long-term stability abroad.

Sometimes understanding how to protect what we earn is just as important as earning it in the first place.

Screenshot of my personal retirement pension record while working in Korea under an F-4 visa as a foreign employee.

What Happens If a Foreigner Leaves Korea Permanently?

Another question many foreign workers may have is this:

What happens to the retirement pension if you stop working in Korea and return permanently to your home country?

In many cases, foreign employees may receive the accumulated retirement pension as a lump-sum payment after leaving the company, depending on the pension type and applicable regulations.

For National Pension, the rules can differ depending on the worker’s nationality and whether Korea has a social security agreement with that country. Some foreigners may qualify for a lump-sum refund, while others may maintain pension rights that can later be claimed according to bilateral agreements between countries.

As for DC Retirement Pensions, the accumulated funds are generally preserved in the employee’s retirement pension account. The exact withdrawal process, taxation, and overseas transfer procedures may vary depending on the financial institution and the employee’s residency status after departure.

Because the regulations can differ significantly depending on nationality, visa type, and pension category, foreign workers should confirm the details directly with:

- The National Pension Service (NPS)

- Their employer’s HR department

- The bank or financial institution managing the retirement pension account

For foreign workers trying to build long-term stability abroad – understanding how to protect what we earn is just as important as earning it in the first place.