Cross-border transactions can become surprisingly complicated when the contract, payment flow, and physical movement of goods all occur in different jurisdictions.

One common question in international trading is:

If goods are sold under a Korean contract but never physically enter Korea, does Korean VAT still apply?

Recently, I reviewed a practical case involving exactly this issue.

Transaction Structure

The transaction had the following characteristics:

- A Korean company receives an order from another Korean company,

- The Korean company purchases goods from a Chinese supplier,

- The goods are shipped directly overseas without entering Korea,

- Payment between the Korean companies is made in KRW domestically,

- But the physical movement of goods occurs entirely outside Korea.

Relevant Korean VAT Interpretation

According to Korean tax interpretations, when goods are supplied under a Korean contract but are delivered directly overseas without entering Korea, the actual movement of the goods may be treated as an offshore transaction rather than a domestic taxable supply.

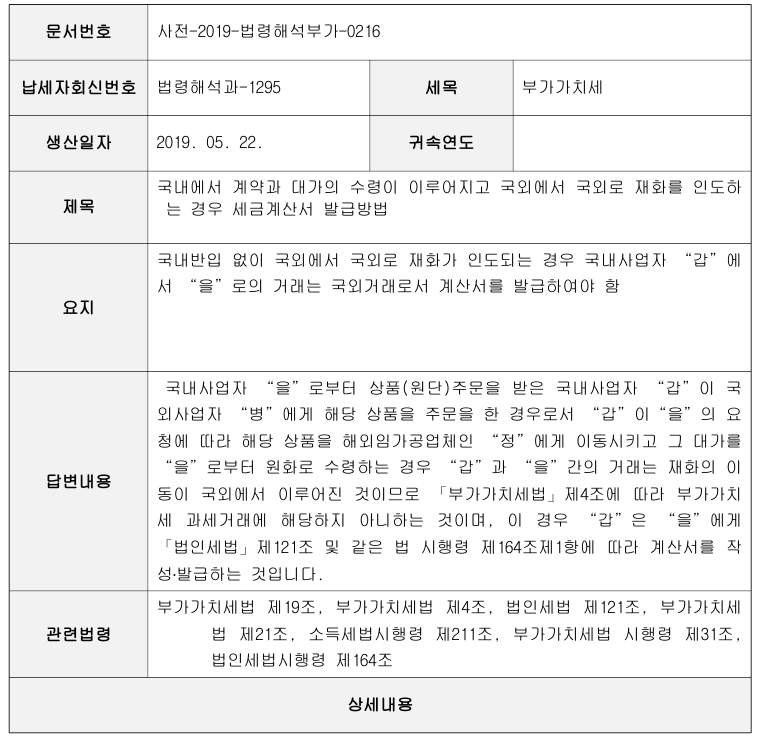

Therefore, the Korean tax authority interpreted that (Reference: 사전-2019-법령해석부가-0216)

- Since the goods never entered Korea and the movement of goods occurred overseas,

- The transaction is not subject to Korean VAT,

- And a regular non-VAT invoice should be issued instead of a VAT (tax typically 10%) invoice.

From a practical perspective, the key issue is not only:

“Who signed the contract?”

but also:

“Where did the actual movement of goods take place?”

Is This Unique to Korea?

Most VAT/GST jurisdictions apply some form of “place of supply” rule.

The general principle is similar worldwide: Consumption taxes are generally imposed in the country where the goods are consumed or supplied.

That is why, if goods never enter Korea, it is generally reasonable that Korean VAT may not apply.

Examples include:

- EU → “Outside the scope of VAT”

- Singapore → “Out-of-scope supply”

- UK → “Outside the scope of UK VAT”

- Hong Kong → No VAT system

- UAE/GCC → VAT determined based on place-of-supply rules

- China → VAT treatment may also depend on the physical movement of goods

However, each country applies its own detailed rules regarding:

- customs,

- foreign exchange control,

- title transfer,

- importer of record,

- VAT registration,

- and permanent establishment (PE) issues.

This is where international trade becomes operationally complex.

Practical China Case

Here is a real-world example showing how logistics, VAT, customs, and foreign exchange regulations can interact in ways that are far more complicated than they initially appear.

Scenario

- Korean Company A wants to purchase product “P” from another Korean Company B.

- Product “P” is manufactured by Chinese Supplier C.

- Company A wants the product to be delivered directly to Company D in China.

- Company D is Company A’s OEM manufacturer located in China.

Based on the earlier explanation, one might initially conclude that this should qualify as an offshore transaction structure.

In other words:

- Company B may be able to issue a non-VAT invoice to Company A in Korean Won,

- while product “P” is delivered directly within China from Supplier C to Company D without entering Korea.

At first glance, the structure may appear simple.

But in practice, another major issue arises:

Can Supplier C deliver the goods domestically within China to Company D while receiving payment from Korean Company B overseas?

The answer is: not so easily.

China maintains strict controls over cross-border foreign currency transactions and export-related payment flows.

If Supplier C receives payment from an overseas entity, Chinese authorities may require the transaction to be structured and reported as an export transaction for foreign exchange and customs purposes.

However, if the goods are physically delivered only within China to another Chinese company, inconsistencies may arise between:

- payment flow

- export declaration

- VAT treatment

- and customs records

In simple terms:

Foreign currency entered China, but the goods never actually left China.

This type of structure can attract regulatory scrutiny because China closely monitors cross-border payment flows, customs reporting, and foreign exchange settlement consistency.

One Possible Solution

One possible structure to address this issue is as follows:

- Supplier C exports product “P” from China to Korea

- The cargo arrives at Busan Port in Korea

- Instead of being customs-cleared for import into Korea, the cargo remains within the bonded area

- The cargo is then re-exported from Korea back to China to Company D

Under this structure:

- Supplier C can legitimately process the transaction as an export transaction under Chinese foreign exchange and customs regulations

- the Korean buyer can justify the overseas foreign currency payment

- Company D can proceed with import customs clearance in China

- and the overall logistics, customs, and accounting flow can remain relatively consistent from a compliance perspective

Although this structure may appear operationally inefficient at first glance, it is sometimes used in practice to align payment flow, customs declarations, VAT treatment, and foreign exchange requirements across multiple jurisdictions.

“If It Only Stays in the Bonded Area, Then Costs Must Be Minimal?”

Many people initially assume this.

“If the cargo never goes through Korean customs clearance and only stays in the bonded area before re-export, then there should be almost no additional costs except shipping, right?”

Unfortunately, not necessarily.

Even when cargo remains inside a bonded area without formal import customs clearance, various operational costs may still apply, such as:

- bonded warehouse charges

- terminal handling charges (THC)

- CFS charges

- documentation fees

- AFR fees

- return customs handling charges

- local transportation costs

- and other port-related operational charges

One interesting point is that local transportation costs may still occur even without customs clearance.

Why?

Because the cargo may still need to be physically moved within the port or bonded logistics system — for example, from an import holding area to an export staging area before re-export processing. In other words, even without import customs clearance, logistics operations themselves still continue.

Final Thoughts

In international trading, reviewing only the contract is often not enough.

In reality:

- VAT,

- customs,

- foreign exchange regulations,

- logistics,

- and bonded warehouse operations are all interconnected.

And that is why real-world international trade operations are often far more complex than they initially appear on paper.